Appearance

能源

LNG (Liquefied Natural Gas): 液化天然气, 气田直接开采,经过超低温液化

LPG (Liquefied Petroleum Gas): 液化石油气, 原油提炼的副产物或天然气加工副产物

- 2026-04-22 全球能源行业 | 因高油价提高盈利而将展望调整为正面,但风险仍存

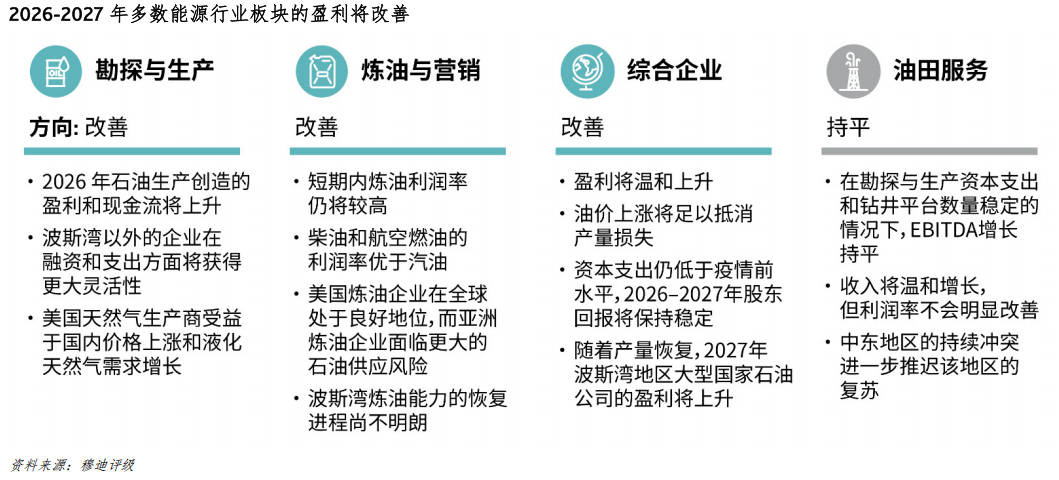

美国炼油企业的利用率较高,裂解价差强劲,原油价差较大,且对中东原油的敞口有限。柴油和航空燃油的裂解价差(即原油成本与成品油销售价格之差)尤为强劲。美国是成品油净出口国,中东地区的供应缩减正在进一步提振需求。缺乏大规模备用产能导致市场供应进一步收紧,并提振了美国炼油利润率。美国释放战略储备等政策措施在一定程度上缓解了原油供应趋紧对炼油企业的冲击。

亚洲的炼油企业经营环境受到更大制约。对中东原油的严重依赖导致炼油企业的供应链受阻,且影响持续时间尚不明朗,这促使许多企业在短期内将重心转向原油采购,并在一些情况下降低加工量。原油库存下降加剧了供应短缺风险。尽管亚洲炼油企业的裂解价差扩大,其已实现盈利能力取决于原油供应的稳定性。价格上限等政策干预限制了炼油企业将上升的成本转移出去。配给措施和可负担性问题也对终端需求形成抑制。部分市场实施的出口限制和关税有助于保障国内供应,但亚洲多数国家缺乏富余产能以供出口。

欧洲的柴油和航空燃油仍呈结构短缺的局面,依赖进口来满足需求。中东冲突引发两类燃料价格飙升,恰逢季节性农业需求上行,凸显了市场的紧张局面。尽管裂解价差处于高位,但在原油成本和运输费用显著上升的背景下,欧洲炼油企业难以显著提高产量。虽然原油库存和战略储备的释放可暂时支持利用率,但结构性限制仍将制约高利润率的实现。

On Friday oil closed at $73 a barrel, the highest since July. This was about $10 above what supply-demand fundamentals would justify, says Tom Reed of Argus Media, a price-reporting agency. At the start of the year many analysts expected an oil “superglut”, caused by rising supply in the Gulf and elsewhere amid tepid demand, to push down prices towards $55 a barrel. In early February the International Energy Agency, an official forecaster, predicted a supply surplus of 3.7m barrels per day (b/d) on average for 2026.

Regional conflict and, in particular, a blockage of the Strait of Hormuz—which carries around 15m barrels per day (b/d), roughly a third of global seaborne flows—could push prices towards $100.

Taking aim at oilfields would be reckless. An Iranian attack on Gulf oil would invite retaliatory strikes from neighbours, which first called for de-escalation.

Hormuz has never been closed to maritime traffic, even during the Iran-Iraq war in the 1980s. Choking it off would antagonise China, which buys nearly all of Iran’s oil and receives 37% of its seaborne crude imports through the Strait.

On February 28th the Islamic Revolutionary Guard Corps (IRGC), the regime’s praetorian guard, broadcast warnings that shipping through the strait was no longer permitted.

Alternative routes are of limited use. Saudi Arabia can redirect barrels via its East-West pipeline; the UAE has a smaller conduit bypassing the strait. Even at full capacity, however, some 8m-10m b/d would remain exposed, estimates Jorge León of Rystad Energy, another consultancy.

Mr Trump could speed things along by tapping America’s Strategic Petroleum Reserve of 415m barrels. That is what Joe Biden, his predecessor, did after Russia invaded Ukraine in 2022. But back then the reserve held nearly 570m barrels. At its maximum draw rate of 4.4m b/d it now would last three months.