Appearance

Circle

STATE OF THE USDC ECONOMY 2025: USDC as a Platform for Global Prosperity

Since its launch in 2018, Circle has bridged more than $850 billion back-and-forth between fiat and supported blockchains.

We have designed USDC using open-source standards and smart contract blockchains so that any developer can easily access the tools they need to build global, scalable digital dollar applications.

While Hong Kong, one of Asia’s most important financial centers, will develop principled rules for stablecoins. These rules will likely build on Japan’s concept of regulatory reciprocity, while adding to Singapore’s longstanding place as Asia’s fintech hub.

Fears of a fierce contest are giving way to collaboration and clarity of purpose, in which today’s generation of stablecoins and blockchain-based financial services are extending – not disrupting – the reach of the real economy.

Mastercard’s partnership with Circle is now entering its fifth year. In 2021, Mastercard announced that it is making it easier for issuers and its Crypto Card partners to use USDC to settle obligations arising from transactions on the Mastercard network. The same functionality was then expanded to support acquirers who want to payout merchants in USDC.

In addition, last year Mastercard introduced a card product construct that enables the spending of USDC held in self-custodial wallets in over 100 million locations where Mastercard is accepted.

USDC

Articles

- 2025-6-3 当稳定币走上风口,“稳定币第一股”周四要IPO了

Investor Relations

- 2025-06-02 S-1/A Securities Registration Statement

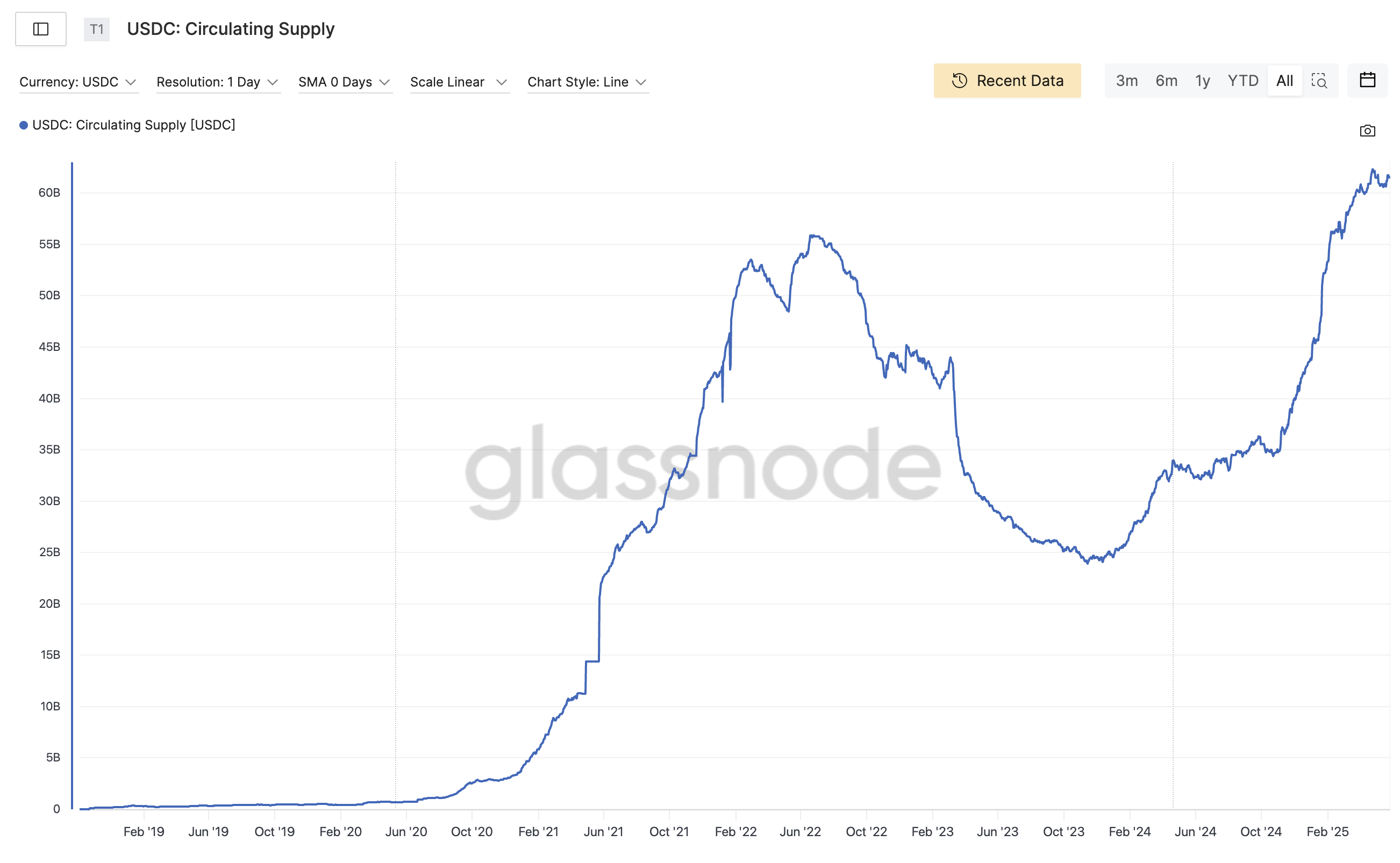

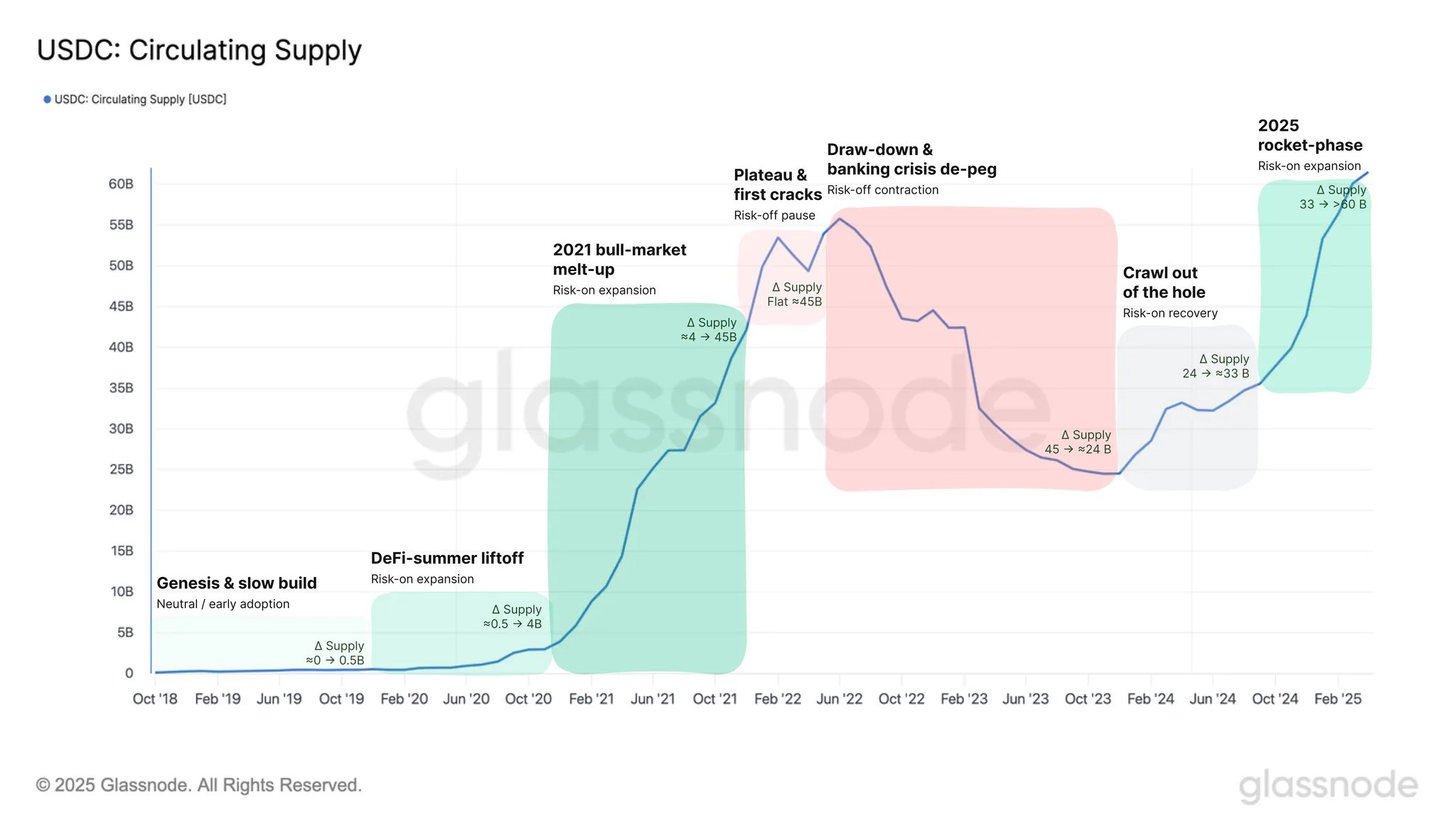

With more than $61 billion of USDC in circulation as of May 23, 2025, millions of end-users use USDC for payments, settlements, and as a digital dollar store of value. Thousands of companies and developers have integrated with USDC, creating a thriving ecosystem. Major payments companies, enterprise technology firms, consumer internet applications, financial technology (“FinTech”) firms, and digital asset companies use Circle technology to power solutions built on USDC.

In 2023, USDC went through an extended period of circulation decline related to a number of factors, including an increase in U.S. short-term interest rates, a decline in digital asset prices, and an associated decline in leverage in the digital asset trading ecosystem, as well as the impact of a temporary price dislocation in the secondary markets in March 2023 resulting from the collapse of certain U.S. regional banks that caused some market share to move to a competitor.

We are building an internet platform company—the Circle stablecoin network provides a platform and network utility with internet-scale reach for consumers and businesses—and a set of software protocols for developers to build and integrate into their own applications. Our business model and technology benefits from network effects that are similar to other leading internet platforms.

2025-04-01 S-1 Securities Registration Statement

Through the partnership, Binance will make USDC more extensively available across their full suite of products and services, ensuring that their more than 240 million global users are able to seamlessly access and use USDC for trading, saving, and payments applications.

Additionally, Binance will adopt USDC as a vital dollar stablecoin for their own corporate treasury, a powerful signal about the world moving on-chain.

Likewise, Circle will provide Binance with the necessary technology, liquidity and other tools for Binance users to benefit from the trust and innovation that Circle has built for USDC. Circle will also work with Binance to build key relationships across the global finance and commerce landscape, as mainstream companies all around the world seek to benefit from crypto infrastructure and stablecoins for an increasingly wide array of use-cases.

Transparency

USDC is a digital dollar backed 100% by highly liquid cash and cash-equivalent assets and is always redeemable 1:1 for US dollars.

The majority of the USDC reserve is held in the Circle Reserve Fund (USDXX), an SEC-registered 2a-7 government money market fund.

The remainder of the reserve is held in cash, mostly among a handful of the world's largest banks with the highest capital, liquidity and supervisory requirements in the world.

Cross-Chain Transfer Protocol (CCTP)

Cross-Chain Transfer Protocol (CCTP) is a permissionless onchain utility that facilitates USDC transfers securely between blockchain networks via native burning and minting.

Payment System

SWIFT

ACH

SEPA

FPS/EDDA

RTGS/CHATS

Markets in Crypto-Asset(MiCA)

Zodia Markets

第一个问题是基础设施,也就是区块链网络本身。

我对区块链网络的思考模型是:它们就像是「互联网的操作系统」。我们需要的是性能更高、吞吐量更强的操作系统型区块链网络。过去这几年,这方面已经取得了很大进步。我们现在已经步入「第三代区块链网络」时代——即高性能的 Layer1 公链,以及 Layer2 扩展网络。

这意味着可以实现更高的交易吞吐量,而且单笔交易的成本极低,可能低于一分钱,甚至不到一美分。

全球范围内,从日本、中国香港、新加坡,到整个欧洲、英国、阿联酋,再到美国,几乎所有主要法域都在陆续推出相关法律,将稳定币明确为合法的电子货币,并将其纳入正式的金融体系。

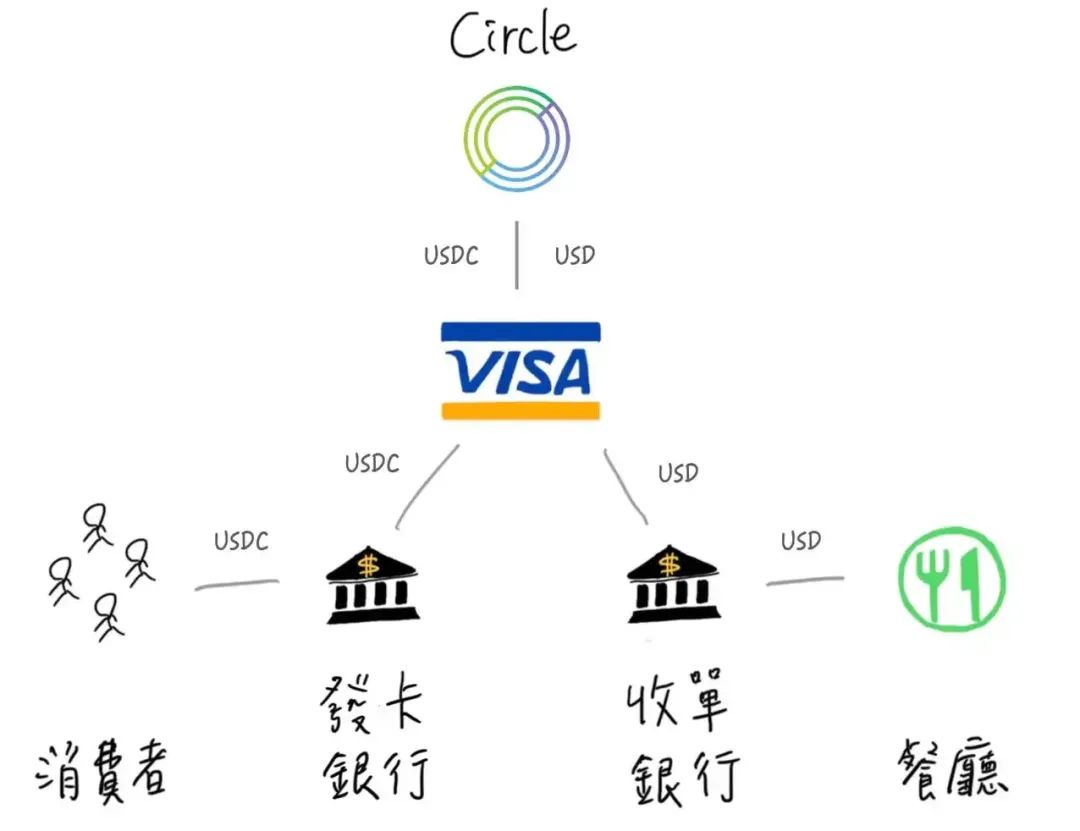

而且现在我们已经在和 Visa 和 MasterCard 展开合作,他们都有项目允许卡片发行机构发行这样一种卡片:表面上是 Visa 或 MasterCard,但实际消费时使用的是稳定币,比如 USDC。

这种模式已经在新兴市场大量涌现,用户通过新银行风格的数字钱包 App 获得一张实体或虚拟卡,这张卡绑定的是他们的稳定币余额。因为很多人希望持有美元,而这些卡让他们可以继续在传统的卡网络中消费,只不过后台清算的方式变成了 USDC。

甚至对于这些卡片发行机构来说,他们向 Visa 或 MasterCard 支付的清算资金,现在也可以直接通过 USDC 来完成。也就是说,USDC 实际上已经被用作金融机构与卡网络之间的清算通道了,这本身就很有意思。

今年年初我们看到一个非常酷的例子:Stripe 联合创始人 John Collison 在他们一年一度的大会上,像往年那样做了一个「压轴发布」,他的原话差不多是:「加密回来了,不过这次不是比特币,而是 USDC,是稳定币。」

他当场演示了 Stripe Checkout 产品中的新功能——这个产品允许商户把 Stripe 的支付入口直接嵌入到自己的网站或 App 中。在演示中,USDC 作为支付方式已经与信用卡并列显示,商户可以选择接收 USDC。

Collison 在台上很兴奋地展示了整个流程,还说:「这才是支付该有的样子。」演示里他们用的是 Solana 网络,结算是实时到账,手续费也非常低。

随着稳定币法律地位的逐渐明确,会有越来越多的金融机构将其视作基础清算层。

比如一个商户可能会说:「我愿意收 USDC,因为我能立刻收到钱,还能省下手续费,对我来说是更好的选择。」

而在用户这一侧,也有越来越多类型的终端产品涌现——不论是传统银行、新兴数字银行,还是加密超级 App,它们都在打造一种无缝式体验,让用户只需扫一扫二维码就能完成支付。

还有一件今年早些时候我在推特上提到的大事:iOS 已经开始开放 NFC 给第三方钱包使用。这意味着,Web3 钱包未来有可能支持「刷手机」支付(Tap to Pay),用户可以直接用手机中装有 USDC 的钱包,在实体商户终端完成支付。

当然,实现这个还需要多方配合,比如支付处理商(Processor)、收单机构(Acquirer)要支持链上交易,钱包开发方要在产品中集成 NFC 功能,还得通过 Apple 的审批。

美国参议院于 5 月 19 日以 66: 32 通过了《2025 年美国稳定币创新指导与建立法案》(GENIUS Act)的程序性投票,试图为美元挂钩稳定币提供联邦监管

Guiding and Establishing National Innovation for U.S. Stablecoins Act.

我们目前在新加坡、欧洲已经获得监管许可,也正在与日本等地合作建立合规的分销渠道,这意味着机构可以在新加坡银行系统、香港银行系统、巴西银行系统、美国银行系统和欧洲银行系统中开设账户并创建或赎回 USDC。

香港稳定币时代加速到来 —— 香港 《稳定币条例草案》立法全速推进